Understanding Default Mortgage Insurance in Canada: What Every Homebuyer Should Know

Buying a home is one of the biggest financial steps you’ll ever take—and for many Canadians, getting approved for a mortgage with less than a 20% down payment means you’ll also need default mortgage insurance. But what exactly is it, why do you need it, and how does it work?

What is Default Mortgage Insurance?

Default mortgage insurance (often called CMHC insurance) is required when your down payment is less than 20% of the purchase price. This insurance protects the lender in case you default on your mortgage—not the borrower.

Three main insurers offer this in Canada:

- CMHC (Canada Mortgage and Housing Corporation)

- Sagen (formerly Genworth)

- Canada Guaranty

Why Is It Required?

Lenders consider loans with smaller down payments riskier. Default insurance allows lenders to approve mortgages with as little as 5% down while minimizing their risk. In return, it gives more Canadians access to homeownership.

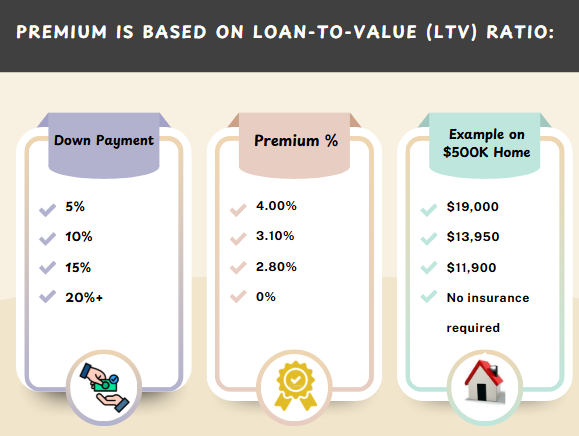

How Much Does It Cost?

The premium depends on the size of your down payment. The smaller your down payment, the higher the premium. Here’s a quick snapshot:

Example:

For a $400,000 mortgage with a 5% down payment, the insurance premium would be $16,000. This is typically added to your mortgage amount, not paid upfront.

Things to Know

- Only owner-occupied properties are eligible.

- Your credit score and debt service ratios still matter for approval.

- Some lenders may choose which insurer they work with.

- Insurance also opens doors to better rates and flexible terms from top lenders.

Still Confused?

Watch the video above to see a visual breakdown of how default mortgage insurance works and when it applies. We explained it all in under 2 minutes!

And if you still have questions about your own mortgage situation—or want to know how much home you can afford—We are here to help.